What is the Asia Pacific Outdoor Power Equipment Market Overview – definition, scope, and significance?

The Asia Pacific Outdoor Power Equipment Market comprises all machinery used for landscaping, gardening, and maintenance of outdoor spaces, including lawn mowers, blowers, chainsaws, trimmers, and related accessories. The scope covers both commercial and residential applications and includes electric‑powered and fuel‑powered equipment. This market is significant because rapid urbanisation, rising disposable incomes, and expanding construction activities in the region drive demand for efficient outdoor maintenance solutions, making it a key contributor to the broader consumer and industrial equipment sectors.

What are the main drivers, restraints, challenges, and opportunities in the Asia Pacific Outdoor Power Equipment Market?

Key drivers include strong housing growth, increased public‑space development, and a shift toward mechanised landscaping. Environmental regulations encourage the adoption of electric‑powered tools, creating opportunities for battery‑technology innovators. Restraints involve high upfront costs of premium equipment and stringent emissions standards for fuel‑powered devices. Challenges stem from fragmented distribution channels and varying regulatory frameworks across countries. Opportunities arise from aftermarket services, smart‑connected equipment, and expansion into emerging economies where outdoor maintenance is still manual.

What growth trends are shaping the Asia Pacific Outdoor Power Equipment Market?

Current trends feature a pronounced shift toward cordless electric models, driven by battery‑cost reductions and consumer preference for low‑noise operation. Smart integration, such as IoT‑enabled diagnostics and remote monitoring, is emerging in premium product lines. Commercial operators are adopting fleet‑management software to optimise equipment utilisation. Additionally, there is an increasing focus on lightweight, ergonomically designed tools that enhance user safety and productivity.

How has COVID‑19 impacted the Asia Pacific Outdoor Power Equipment Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed construction projects, leading to a short‑term dip in commercial orders. However, lockdowns heightened consumer interest in home improvement and garden care, boosting residential sales of lawn mowers and blowers. As economies reopen, the market is experiencing a robust rebound, with growth accelerating in 2024 and beyond, supported by pent‑up demand and continued investment in public‑space maintenance.

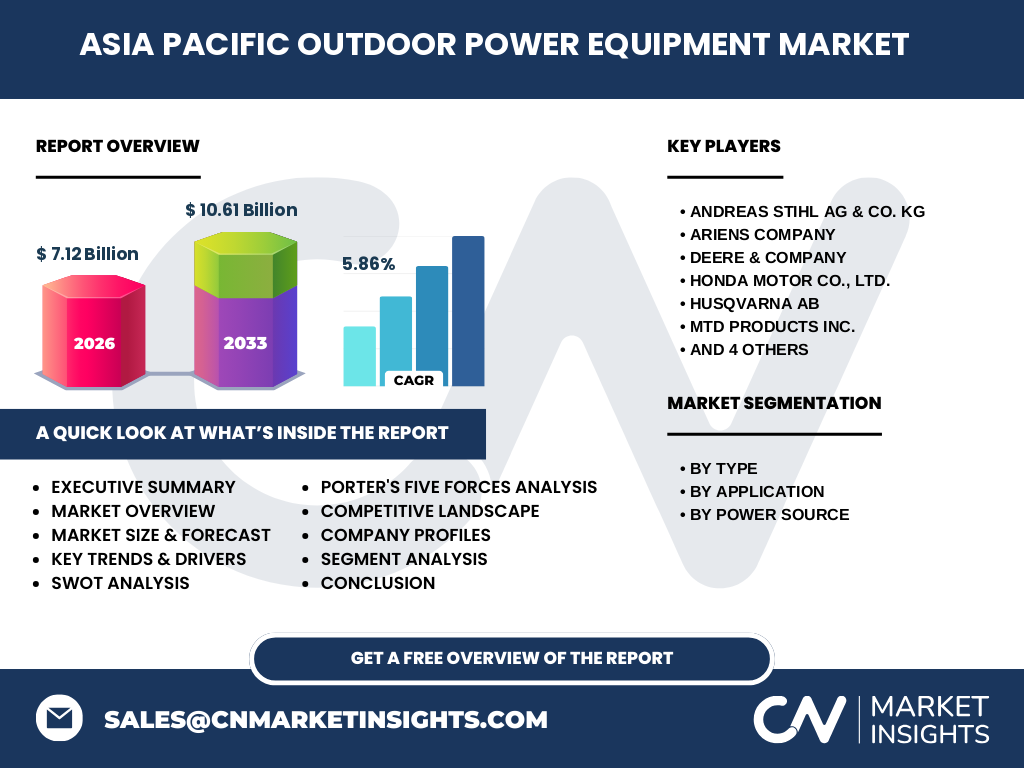

Who are the major competitors and what is the level of market consolidation in the Asia Pacific Outdoor Power Equipment Market?

Leading firms include ANDREAS STIHL AG & Co. KG, Ariens Company, Deere & Company, Honda Motor Co., Ltd., Husqvarna AB, MTD Products Inc., Robert Bosch GmbH, Techtronic Industries Co. Ltd., The Toro Company, and YAMABIKO Corporation. The market exhibits moderate consolidation, with a few global brands commanding significant share while numerous regional players serve niche segments. Recent mergers and strategic alliances are aimed at expanding product portfolios and strengthening distribution networks.

What are the high‑level insights and key findings from the executive summary?

The Asia Pacific Outdoor Power Equipment Market is valued at USD 7.12 billion in 2026 and is projected to reach USD 10.61 billion by 2033, representing a CAGR of 5.86 % over the forecast horizon. Growth is propelled by urban expansion, rising consumer spending on home landscaping, and a transition toward electric‑powered tools. Competitive dynamics are shaped by technology‑driven product differentiation and strategic partnerships. The market outlook remains positive, with ample scope for innovation and expansion in both commercial and residential segments.

What are the forecast expectations for the Asia Pacific Outdoor Power Equipment Market through 2025‑2032?

Based on the provided CAGR of 5.86 %, the market is expected to continue expanding steadily, reaching close to the 2033 forecast of USD 10.61 billion. Growth will be supported by increasing adoption of battery‑electric equipment, deeper penetration in emerging economies, and ongoing infrastructure projects that require reliable outdoor power tools. Seasonal demand cycles will remain, but overall annual growth will stay above the mid‑single‑digit level.

How is the market size and share distributed by segmentation (type, application, power source)?

Segmentation by type showcases a diverse product mix: lawn mowers, blowers, tillers & cultivators, chainsaws, trimmers, hedge trimmers, sprayers, and mist dusters. Application segmentation splits the market into commercial and residential uses, with residential demand driving volume growth and commercial contracts contributing higher average selling prices. Power‑source segmentation reveals a clear bifurcation between electric‑powered and fuel‑powered equipment, with electric models gaining market share due to environmental incentives and lower operating costs.

What is the geographic distribution of the market size and share within the Asia Pacific region?

The market is broadly distributed across key sub‑regions, including East Asia, Southeast Asia, and South Asia. Economies such as China, Japan, South Korea, India, and Australia account for the majority of the market’s revenue, reflecting their high levels of urban development and mature consumer bases. Emerging markets like Vietnam, Philippines, and Indonesia are witnessing faster growth rates, contributing increasingly to the overall regional share.

What are the detailed regional performance trends in the Asia Pacific Outdoor Power Equipment Market?

East Asia leads in unit sales, driven by advanced manufacturing capabilities and strong demand for high‑tech electric tools. Southeast Asia shows rapid adoption of cost‑effective fuel‑powered equipment, though electric penetration is accelerating with government incentives. South Asia, particularly India, displays robust residential demand as homeowners invest in garden maintenance. Australia’s market is characterised by premium‑segment growth, with a notable shift toward battery‑operated lawn care solutions.

Which leading companies operate in the Asia Pacific Outdoor Power Equipment Market and what are their core strategies?

Key players such as ANDREAS STIHL AG & Co. KG and Husqvarna AB focus on brand strength and product innovation, launching cordless premium lines. Honda and Yamaha leverage their engine expertise to dominate fuel‑powered segments while expanding electric offerings. Techtronic Industries and The Toro Company pursue aggressive acquisition strategies to broaden portfolio breadth. MTD Products and Ariens concentrate on value‑priced models for the residential market, emphasizing distribution reach.

How does Porter’s Five Forces framework apply to the Asia Pacific Outdoor Power Equipment Market?

• Threat of new entrants is moderate due to high capital requirements and brand loyalty. • Bargaining power of suppliers is relatively low because components such as batteries and engines are sourced from multiple vendors. • Bargaining power of buyers is high in the residential segment, where price sensitivity drives competition. • Threat of substitutes is low, as outdoor power equipment remains the primary solution for landscaping tasks. • Competitive rivalry is intense, with global brands competing on technology, price, and service networks.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths: Established brand portfolios, wide product ranges, and strong distribution channels.

Weaknesses: Dependence on cyclical construction activity and high R&D costs for electric technology.

Opportunities: Expansion of electric and smart‑connected tools, growth in emerging economies, and aftermarket service revenue.

Threats: Regulatory tightening on emissions, raw‑material price volatility, and intense price competition.

What does the value chain analysis reveal about the industry structure?

The value chain begins with raw‑material suppliers (metals, plastics, batteries), followed by component manufacturers (engines, electric motors). These feed into original equipment manufacturers (OEMs) that assemble and brand the final products. Distribution includes wholesale distributors, specialty retailers, and e‑commerce platforms. After‑sales service, spare parts, and refurbishment form the downstream segment, offering additional revenue streams and customer loyalty opportunities.

What key investment insights can be drawn for investors looking at the Asia Pacific Outdoor Power Equipment Market?

Investors should target companies with strong electric‑power technology pipelines and robust after‑sales networks. Partnerships that enable local market penetration, especially in high‑growth Southeast Asian nations, present attractive upside. Monitoring regulatory trends can help identify early‑stage opportunities in low‑emission product lines. Acquisition of niche service providers can enhance profitability through recurring revenue.

What are the main conclusions and take‑aways from the market analysis?

The Asia Pacific Outdoor Power Equipment Market is on a steady growth trajectory, underpinned by urbanisation, rising consumer affluence, and a clear shift toward electric‑powered equipment. While competitive pressures are high, companies that innovate in battery technology, digital connectivity, and service solutions will capture the largest share of future gains. Regional differences underscore the need for tailored strategies that address local preferences and regulatory environments.

How was the research methodology designed and executed?

The study combined primary interviews with industry experts, OEMs, and distributors, alongside secondary data from company reports, trade publications, and government statistics. Market sizing employed a top‑down approach using the provided 2026 baseline and forecast figures, while segmentation analysis leveraged product‑level sales data. Trend forecasting applied compound annual growth rate (CAGR) calculations and scenario modeling.

What is the defined scope of the research and its boundaries?

The scope covers all major outdoor power equipment categories sold in the Asia Pacific region, encompassing both commercial and residential applications and both electric‑ and fuel‑powered variants. The analysis excludes unrelated agricultural machinery and focuses on the period up to 2033. Geographic coverage includes all Asia Pacific countries, with deeper emphasis on markets where data availability is strongest.

Which key companies and recent developments have shaped the Asia Pacific Outdoor Power Equipment Market?

Notable players such as ANDREAS STIHL AG & Co. KG launched a new line of high‑capacity lithium‑ion cordless mowers, while Honda introduced a hybrid engine model for chainsaws aimed at reducing emissions. Techtronic Industries announced a strategic partnership with a regional e‑commerce platform to expand online sales channels. The Toro Company rolled out a connected‑equipment platform that offers predictive maintenance analytics for commercial fleets. These developments illustrate the industry’s focus on electrification, digital integration, and channel diversification.